Barriers, Priorities, and Focus on the Consumer: a Snapshot of New Activity in the Texas Virtual Power Plant Project

ADER project updates from July through August 2024, and how to make sense of aggregators, retailers, and customer choice for VPP in Texas.

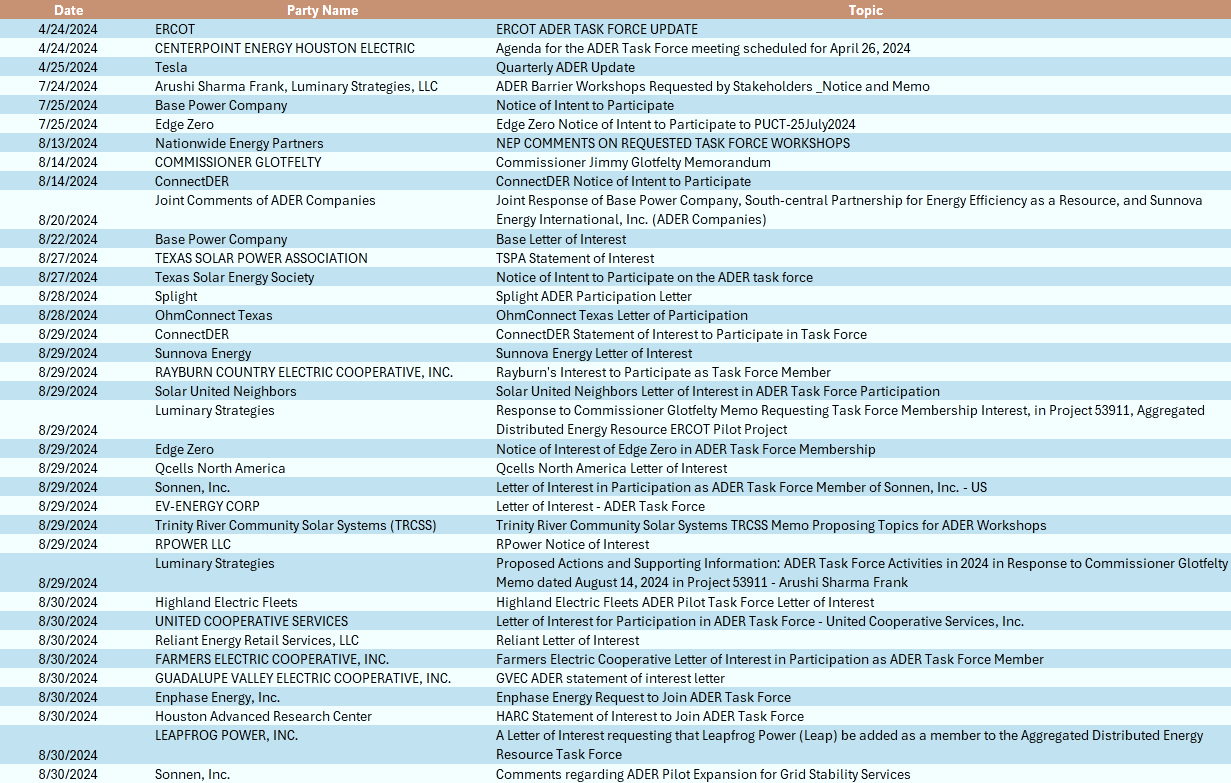

The Texas #ADER Task Force Project 53911 is seeing a flurry of activity, beginning with the date that I filed on behalf of stakeholders in ERCOT Texas, a list of barriers to Virtual Power Plant growth in Texas. Check this out:

Come back for more next week. For now, you should walk away knowing that the issues assigned to the Task Force to solve in a memo from Commissioner James Glotfelty on August 14, 2024 require the task force to take on some interesting questions. Digesting this memo and the other pending work to be done, I filed a list of priorities to help support the group’s future consensus on how to tackle each area and on what timeline. You have got to hand it to them: this group works hard, on top of their day jobs, to make #DERs a reality for Texas.

One standout item: it is amazing and rewarding, and timely, to see interest finally from Original Equipment Manufacturers in participating in this project. I have been very concerned that companies which do not actually make the product, but want more customer accounts or more participation in the pilot (neither are bad, we want to grow everyone’s business and opportunity) are the only parties who have been talking about difficult topics like open APIs and regulatory mandates for technical voluntary standards.

I am also concerned about confusion on the topic of customers being able to “freely choose” their VPP provider as the potential fix to grow participation. That is not the fix: it is increasing the ease of access to more grid services that fit technologies which customers invested in so that more retailers can help customers monetize their systems. This will take work from ERCOT, primarily, and secondarily from their regulator. Some ADER providers have been limited in market participation due to level 4 QSE operational costs associated with the ERCOT Pilot Phase I and Phase 2 requirements related to grid services (nonspin and ECRS) delivery. If new grid services like block load response can allow for lower-cost QSE enablement, existing ADER providers and new ADER providers will be able to initiate ADERs outside Houston (a concern described in the August 14, 2024 memo). The memo also called for "a roadmap for the commission on how we get to eighty MWs of participation and what is next beyond that." ERCOT SCED dispatch is the only option for ADER resources today, and it is costly. So much so, that even a company with active ADERs today has presented multiple times at Task Force meetings that the current provisions of the ADER pilot tied to such costs and complexities are a barrier to its own expansion and to the market entry of others. (This party was Tesla, Inc.).

We have to build awareness in the weeks that come, that when VPP services and equipment are purchased together, policy should never seek to break privity between a customer and its DER aggregator which bundled the sale of a DER device at some discount for the customer, attached to the aggregator’s grid services platform agreement. Such agreements accompany the sale of the device(s), and are not tied exclusively to a customer’s choice of competitive electric provider. Our markets for VPP and #DER exists today largely because of contracts and commercial opportunity to package hardware and services together. This packaging builds a strong relationship of trust with a customer, on top of the contractual obligation, that the extra device control discretion the aggregator gets back, is going to be well-managed. It also ensures hardware will not be exposed to cyber risk or other vulnerabilities. VPP programs in utility and non-utility areas all have gatekeepers ensuring that hardware participation in a program is paired with a dedicated, high-quality set of DERMs/aggregation platform providers. Programs do not allow random switching of equipment or service provider in these programs; customers have to relieve themselves of the program if they make those switches. In Texas, a totally unique space in terms of market design, this can get tricky, so it is important to understand what is at stake. [Some retailers can also offer a specific device or class of devices, and only that device class and no other accompanies a special rate or offer they can exclusively provide, because they built a business model to deliver their view of the best customer value to the market].

Comparative analogy to other consumer bundled products and services may help your thinking as it has helped mine. If I buy new audio software and hardware system with advanced, auto-updating features needing ongoing servicing, I would like the parties who service it and update those features to do their best: that is likely to be the entity that sold it or its contracted affiliate which has spent time, money, and built the right connectivity between vendors to not screw up. Between these parties, there is also comfort for me as a consumer that there is oversight and regulatory accountability because they gave me a contract and bound themselves to me - and if it sucks, I’ll post about it. Also, the parties in that contract share and price in risks around eating the costs of failure, and then offer me a better deal: if they did not, I would pay more at the outset for unbundled hardware and software, or, I’d pay more when something goes wrong with either, and bear that cost myself.

So what if there was a third party servicer that is not the entity group I got my bundled product from? That party better know what it is doing, and they will have a monopoly on me if they are the only party out there seeing value in providing that service to me. A monopoly on my business - but, no accountability or reputation risk associated with the brand name of the product I bought: I would feel better with a third party servicer if there was a deep, liquid market for after-market services for my product with plenty of trust and accountability baked in. Also, I would be more likely to go to an after-market servicer if I knew real facts about the quality of their experience and depth of expertise with my device.

Another consideration for policymakers and consumer protection: with an expensive audio system maybe I want to take the risk of going with a third party servicer. Do I want to take the same risk of breaking my service contract with the entity I got my home backup power from?! One item is a luxury, the other, a necessity. It is definitely more likely I will choose to avoid a potential screw up from a third party servicer of my home power source.

My hypothetical sound system bundle of hardware and software is a Toyota, my home power system and bundled aggregator service is a Ferrari. (’We’ve got one of those somewhere in the family - the car, not the VPP plan. There is one servicer in my tri-state area that is a non-Ferrari provider of maintenance and repair. Owners take their cars there for some repairs (the routine things they would like to pay less for), but, they go only to the Ferrari dealership for the critical stuff.)

Back to ADER: we are not articulating yet, and need to, that contractual privity and the commercial opportunity that comes with it is driving uptake of resiliency faster and more affordably.

Whether you are an aggregation services provider with third-party solar-batteries to sell or lease to customers, or a manufacturer that has integrated a specific provider’s platform access into device firmware, or a retailer that has both the software and the product manufacturing in the same family of services through vertical production or vendor contract, it is the job of the market to decide which models will “win” in Texas. Ideally, many win together, which is why creating more grid services access must be the top priority of the ADER Task Force.

We should not - and cannot - use regulatory tools to change commercial relationships that have become the backbone of how consumers get access to the best and greatest products and services in the first place. Instead we build market opportunities to increase the VPP value pie. Increased product and service choices, switchability, and market liquidity will follow. Companies must compete to provide the best overall experience to customers, and the customer’s choices are never infinite because less attractive and valuable options do not make it. That is what sensible free market regulation is for: putting basic guardrails in place to limit price gouging or other unethical outcomes, and letting the market decide who will show up with the best products and services. You can read more about that in my filing. Do scroll the list of participants interested in ADER task force participation, to understand many of them have a VPP business model that is somehow contingent on contractual privity with a customer.

Here is my list of proposed priorities from that filing about what the ADER Task Force should focus on in the few months remaining this year, and beyond.

- Arushi Sharma Frank